As the saying goes, "blessings and misfortunes come together, crises and opportunities coexist." Beyond the shadow of the early-year "T86 tariff war" crisis, the U.S. e-commerce market across the Atlantic is also brewing an even more astonishing opportunity explosion.

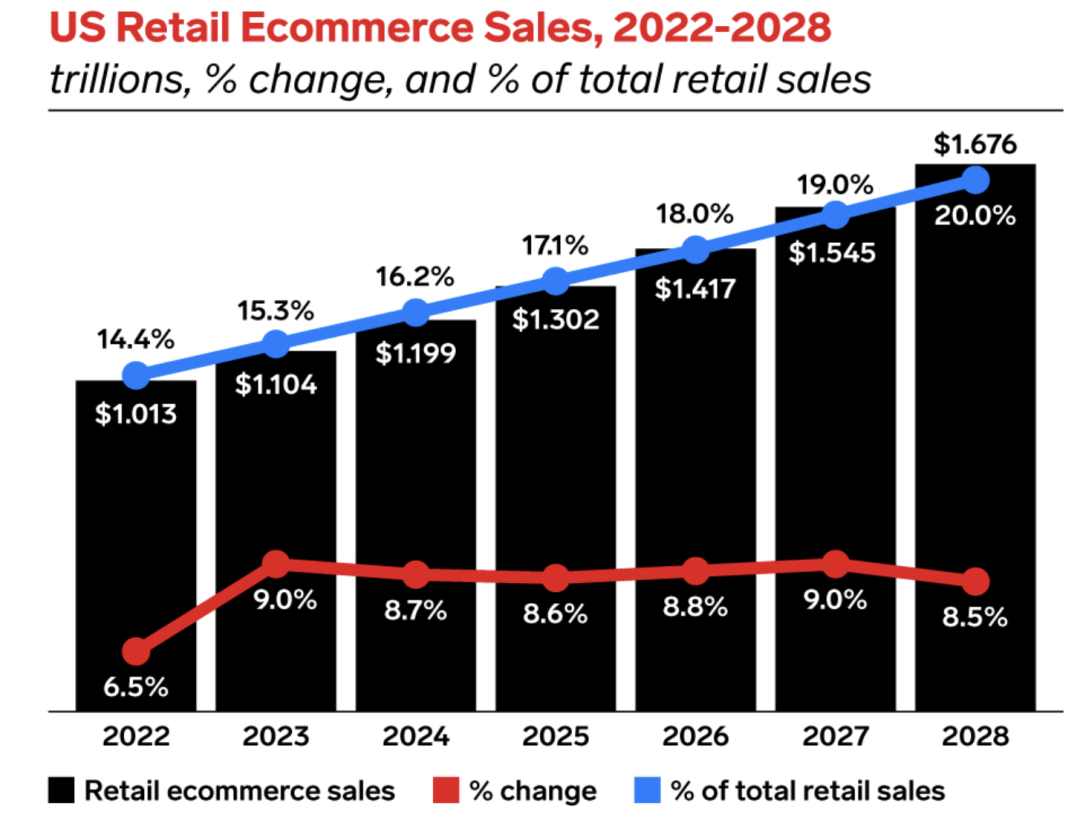

According to the latest forecast from eMarketer, the U.S. e-commerce market will capture nearly $1 trillion in incremental growth between 2024 and 2028. This figure is quite substantial, effectively securing the growth prospects of the U.S. cross-border e-commerce market for the next few years and providing a strong sense of reassurance for cross-border sellers.

More importantly, e-commerce growth will outpace brick-and-mortar retail by an absolute margin of four times. By 2028, one out of every five dollars in retail spending will come from online channels.

The growth rate and penetration of e-commerce are both overwhelmingly ahead of offline retail.

Key Data Snapshot:

Healthy overall growth: E-commerce grew 8.7% in 2024, with total market size approaching $1.2 trillion.

Mobile share rising: Mobile shopping is becoming more common and is expected to surpass the 50% mark by 2028.

Buyer demographic shift: Among new online shoppers, Generation Z will account for 90% of consumer contributions.

01

"The Online Counteroffensive": Three Key Turning Points for U.S. Cross-Border E-Commerce

In the early post-pandemic period, offline consumption in the U.S. quickly rebounded, causing the online penetration rate that had accumulated during the pandemic to decline. However, over the past two years, the U.S. cross-border e-commerce market has been staging an "online counteroffensive":

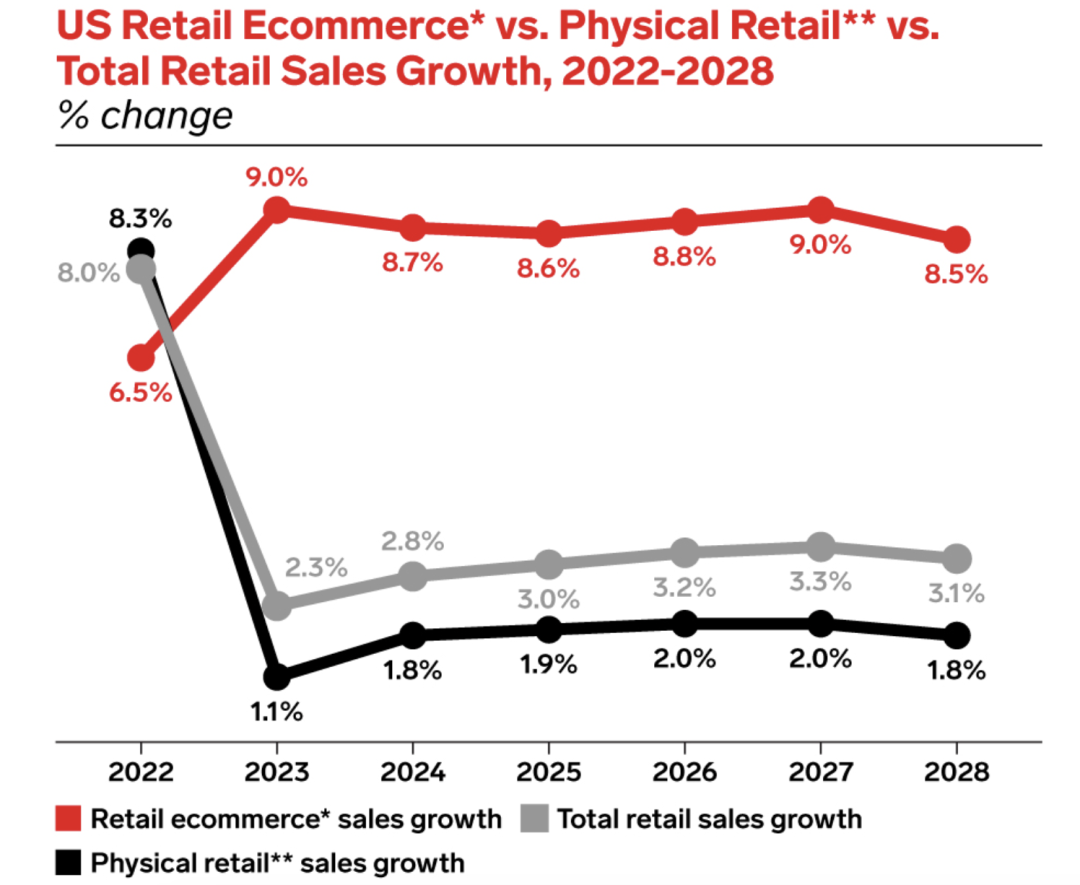

Currently, while offline stores still account for 80% of retail sales, their growth has stagnated at around 2%. In contrast, e-commerce, even without the pandemic tailwind, has maintained a steady growth rate of 8.5%-9% annually. This stable growth represents a promising future for cross-border e-commerce sellers.

Behind this steady growth, a closer look reveals three key turning points:

First, mobile shopping has become the new normal: By 2028, mobile devices will contribute two-thirds of e-commerce growth. Young people even place orders directly through TikTok, a stark contrast to their parents' generation, who are accustomed to ordering on desktop computers.

Second, cross-border e-commerce has entered an era of greater cost-effectiveness, with price wars intensifying. Since the entry of Temu and SHEIN, online prices for apparel and electronics have generally fallen by 5%-9%. This proves that no one can resist the allure of high-quality, low-priced goods.

Third, consumer habits are irreversible. The "lazy economy" cultivated during the pandemic is still fermenting. 70% of users say they will continue to increase their proportion of online shopping. For example, 3C electronics purchased during the pandemic are now due for replacement, which will drive another wave of consumption.

Looking ahead, these three "engines" are accelerating, driving e-commerce penetration to exceed the 20% mark.

Although the U.S. started e-commerce early, due to infrastructure and other factors, online penetration remained around 15% for a long time.

Now, with all three engines firing simultaneously, U.S. e-commerce penetration is expected to historically break through the 20% threshold by 2028, effectively increasing by one percentage point per year.

Behind this are three "engines" familiar to Chinese enterprises going global:

Engine 1: Mobile Revolution

By 2028, 94% of online transactions are expected to be completed via mobile phones. Social commerce is emerging rapidly. For example, TikTok Shop's single-day GMV has exceeded $10 million. In-app closed-loop is becoming standard, with Amazon and Temu both enhancing their "see now, buy now" features to shorten buyers' purchase decision cycles.

Engine 2: Generation Z Awakening

This "mobile-native generation" accounts for 90% of new online shoppers. Unlike their parents, their purchase decision paths have changed dramatically. 38% complete their entire journey from discovery to purchase directly on social media platforms. Impulse buying has increased, driven by the mentality of "buy early, enjoy early." They are also more price-sensitive, with 73% comparing prices across the web before making a purchase. It's not about whether it's cheap; it's about not paying too much.

Engine 3: Category Structure Evolution

Among popular categories for cross-border e-commerce brands going global, high-frequency categories such as apparel and beauty have seen online penetration exceed 35%. The toys category has emerged as a standout, with online penetration expected to surpass 50% by 2025. The home and furniture category is also making a comeback: after several years of stagnation, large furniture is growing at an annual rate of 9.2% online, far exceeding the industry average.

02

The Trillion-Dollar Market Battle: Overseas Warehousing as a Core Competitive Advantage

In the seemingly monolithic U.S. market, a "battle for a new king" in cross-border e-commerce is unfolding. Although Amazon still reigns with a 40% market share, the rise of Chinese global brands is accelerating at a rate that cannot be underestimated.

Amazon's FBA overseas warehouse "moat" remains significant, with net sales of $638 billion in 2024, Prime membership penetration exceeding 65%, and a logistics network covering 98% of the U.S.

Chinese value-for-money platforms are conducting a blitzkrieg, with daily parcel volumes exceeding 800,000. Apparel prices are 30%-50% lower than local platforms, and customer acquisition through social media referrals has been remarkably effective.

TikTok Shop's content e-commerce model is a disruptive force. Average user session duration exceeds 90 minutes, with conversion rates 3-5 times higher than traditional platforms. KOL live-stream selling has become standard for "social media content e-commerce."

What should give us pause is that this "contest" is not just about platform market share; it is also reshaping the rules of the game for U.S. e-commerce:

· Logistics Speed Battle: Amazon's "same-day delivery" faces value-for-money challenges from platforms like Temu. Some pay for faster delivery, while others pay for lower prices.

· Content Marketing Battle: Short-video "seed planting" is replacing traditional search-based shopping. From "you want to buy" to "recommended for you," intelligent recommendations will fundamentally change traditional purchase decisions.

· Overseas Warehouse Stealth Battle: Chinese sellers, leveraging overseas warehouses, have compressed fulfillment times to three days. Large overseas warehouse service providers in the U.S. have already exceeded one million square meters in area, enabling multi-warehouse regional fulfillment and short-chain delivery times that rival Amazon.

03

Changes Amidst Certainty: Three Survival Rules for Going Global

Facing a trillion-dollar market opportunity, those who want a piece of the pie must master the new rules:

Rule 1: Data-Driven Product Selection, Target High-Growth Sectors

Apparel, home, and toys are leading the incremental market with 60% annual growth. Despite cost pressures from the tightening of the T86 customs policy, the extreme value-for-money barrier of China's supply chain remains difficult to shake. Traditional offline categories such as auto parts and fresh food, against the backdrop of ongoing global inflation, are making a comeback on the logic of "online replacing offline." U.S. consumers are willing to wait three more days for a 30% price advantage. Cross-border sellers need to deeply explore the "essential value-for-money" niche.

Rule 2: Localization is Not a Choice, But a Bottom Line for Survival

Although the T86 drama has temporarily subsided, the Sword of Damocles still hangs high. Once U.S. Customs completes its transition period, the $800 de minimis policy is likely to be tightened. As the advantages of direct shipping diminish, stocking goods in overseas warehouses remains an essential choice for cross-border e-commerce.

Rule 3: Mobile Experience, The Next Generation Shopping Gateway

What you've played with domestically can be played again in cross-border e-commerce. A new generation of young buyers has arrived. The advantages of traditional web-based shopping will slowly fade. Young users don't just want "the ability to buy"; they want an "immersive shopping experience," enjoying discounts within refined apps rather than being overwhelmed by web versions.

Although last year's TikTok storm has not yet passed, content e-commerce has taken root in the hearts of young people. Once a seed is planted, it is not easily erased. Mobile shopping represents a more advanced shopping model, more aligned with the consumption concept of the new generation of young people.

Over the next five years, amidst certainty, there will also be changes. Standing at the threshold of 2024, we believe the U.S. e-commerce market will present two major certainty trends and three variables:

The Matthew Effect will intensify: Top platforms will eat up 80% of the incremental growth. Players need to find their own ecological niche.

Local advantages will expand: The era of heavy tariffs is coming. Localized overseas warehouses will become a standard feature for going global.

Three variables:

The release of consumer spending power driven by Fed rate cuts; AI technology changing shopping comparison models; and changes in tax policies related to cross-border e-commerce.

For Chinese sellers, the U.S. market, growing at an average annual rate of 8%, is both a gold mine and a testing ground. Players who quickly adapt to the new triangular relationship of "mobile shopping + social referral + local fulfillment" will be able to cut the most generous slice of the trillion-dollar pie.