In the past, robbery was "this road is mine, pay the toll to pass." Now, robbery is "welcome to the Port of New York, please pay $1 million in service fees."

Yes, the United States has done it again:

Recently, the U.S. Section 301 investigation bill targeting China's maritime, logistics, and shipbuilding industries proposes to impose a sky-high "port service fee" of up to $1.5 million per vessel per port call.

This isn't a port — this is highway robbery.

The bill is based on the 50-year-old Trade Act and was initiated by the Office of the U.S. Trade Representative (USTR), which is under the Executive Office of the President. From five U.S. unions applying to launch a Section 301 investigation last April, to the USTR releasing a 165-page investigation report in January this year, then announcing specific fee structures and mandating "U.S. goods on U.S. ships" in February, ending public comment on March 10, holding a hearing on March 24, and submitting to Trump for approval one week after the hearing — it could be implemented as early as April.

For the U.S., where deliberations often take one to two years, this efficiency is simply astonishing.

T86 just finished tormenting air freight, and now Section 301 is coming for sea freight. Only three months into 2025, and it's already more eventful than the past three years combined.

(Reply "Report" in the official account dialog to receive for free: the original bill + in-depth interpretation + 8 detailed reports)

01

Fee Structure: How Will the Sky-High "Port Service Fee" Be Charged?

The USTR wrote a lengthy 165-page report. Let's skip the groundwork and focus directly on the "fee structure." In summary, it's "three additions and one subtraction."

Simplified Fee Structure, Created by Gucang, Click to Enlarge

(1) For Chinese shipping companies:

$1 million per vessel per port call; or $1,000 per net ton.

Note that this is a "choice of one" between the two options, applying to "all vessels" of Chinese shipping companies, regardless of whether the vessel was built in China.

For example, for an 80,000-ton Panamax container vessel from China, the tonnage-based fee would be $80 million, but the port has "thoughtfully" set a cap of $1 million, so the port service fee would be $1 million.

A question arises: if a vessel calls at a port in the southern U.S. and then calls at a port in the eastern U.S., will it be charged twice? The right to interpret these nuances belongs to the USTR.

(2) For shipping companies from other countries:

a. For vessels built in China, up to $1.5 million per vessel per port call;

b. Tiered fees based on the proportion of "Chinese-built vessels" in the fleet: over 50% = $1 million per vessel; 25%-50% = $750,000 per vessel; below 25% = $500,000 per vessel;

c. In addition to the above two points, there is also a straightforward calculation: if the share of "Chinese-built vessels" in the fleet exceeds 25%, a flat fee of $1 million per vessel applies.

It is important to note that if a shipping company has 100 vessels, only one of which is Chinese-built, and that vessel does not serve U.S. routes, the remaining 99 vessels would still be subject to a $500,000 fee per port call — a modern version of collective punishment.

(3) For shipping companies that order new vessels from China within the next two years:

Tiered fees based on the "China content" also apply, following the same standards as point (2) — no further elaboration needed.

This measure is primarily aimed at blocking new ship orders. The issue is that the bill does not specify whether items (1), (2), and (3) are cumulative. So, in theory, fees could be "stacked": for example, if a foreign shipping company with 100 vessels, 70 of which are Chinese-built, also orders 10 new Chinese-built vessels, a single port call could incur a fee of $1.5 million or $1 million + $500,000.

(4) Fee Reductions and Benefits

"U.S. version of a tax rebate" — if a shipping company uses a U.S.-built vessel, it may receive a refund of up to $1 million in service fees each time that vessel enters a U.S. port.

Additionally, the USTR announced an "8-year plan for shipping U.S. goods on U.S. vessels": starting in 2024, 1% of U.S. exports must be shipped on U.S.-flagged vessels, increasing to 3% by 2027 and 15% by 2032.

However, the reality is that in 2025, the U.S. has only about 70 commercial vessels capable of international routes, with 0.1% of new ship orders. China has over 2,000 commercial vessels, accounting for 74.1% of new ship orders.

Closing such a massive gap within eight years — even Nuwa working overtime couldn't patch that up.

02

Explosive Reactions: The Freight Rate and Profit "Scissors Gap"

If this bill is submitted to Trump and approved in April, the ripple effects could be even more explosive than T86, given that sea freight accounts for 80% of global transportation, with Asia-U.S. routes making up a large portion of that.

1. Surging First-Mile Costs:

Historically, shipping companies cannot absorb these sky-high port fees and will most likely pass them on to cargo owners. Combined with new tariffs after the New Year, shipping costs will double while price increases remain difficult, especially affecting price-sensitive buyers. Moreover, to avoid cumulative fees, shipping companies will inevitably reduce port calls, which would require more feeder vessels, generating new transshipment costs.

2. Reduced Maritime Capacity:

To avoid the fees, shipping companies will need to redeploy vessels and adjust routes, but this would take one to two months to complete. This is especially critical for U.S.-China routes, which coincide with the Q2 peak sea freight stocking season. Rising demand coupled with reduced capacity could lead to freight rate increases, tight container space, cargo delays or loss, impacting sales cycles and buyer experience.

3. A New Wave of Stockpiling:

Similar to last year's East Coast port strike and Trump's tariff threats, when signs emerge or the probability increases, cargo owners tend to stock up early to avoid costs, driving a new round of competition for first-mile capacity and warehousing resources. For example, last year some sellers anticipated tariff increases and stocked up in advance, successfully avoiding two rounds of post-New Year tariff costs.

4. Disruption of Long-Term Contract Rates:

Although overall sea freight rates have been trending downward after the New Year, and the new shipping alliance structure is not conducive to rate increases, if the port fee is implemented in April, it could disrupt 2025 contract rates. Most U.S. route contracts are finalized between January and April, while the hearing is in March. Shipping companies may incorporate this fee into negotiations, pushing long-term contract rates higher against the trend.

5. Renewed Supply Chain Turmoil:

To save on U.S. port service fees, the only alternative is to divert via Mexican or Canadian ports, unload there, and then transport the goods into the U.S. by rail or truck. However, aside from the question of whether Mexico and Canada can handle this surge in volume, land transport costs are several times higher than sea freight. Given the vastness of U.S. territory, distances from north to south and south to north are enormous, making both timeliness and cost difficult to control. Moreover, if port volumes in the U.S. decrease, longshoremen might go on strike again.

In response, MSC has warned that if the port fees are indeed implemented, container freight rates could soar by 25%, forcing the company to adjust its network and reduce coverage, passing the additional costs on to consumers. Drewry analysis indicates that over 80% of container vessels currently calling at U.S. ports would be affected, with per-container costs increasing by $222-500 — a disaster for the shipping industry.

So, is this truly unsolvable?

03

Future Direction: Extreme Uncertainty for the "Port Fee"

Under U.S. law, the bill has reached the hearing stage, which will be followed by a week of public comment. Since it is a hearing, there will be opposing views, especially since U.S. importers and economists are not foolish. Even if the hearing passes, it must be submitted to Trump in April for his signature to take effect.

In terms of feasibility and likelihood, the implementation of the "port service fee" bill is highly uncertain.

First, the U.S. shipbuilding industry is beyond saving.

Currently, 74% of global new ship orders are held by China, while the U.S. holds less than 0.1%. The U.S. cannot even build five vessels of over 10,000 tons per year, and prices are exorbitant: an 180,000-ton bulk carrier costs $120 million from China but $500 million from the U.S., with an additional two-year wait for delivery.

For the U.S. shipbuilding industry to revive, it would not only require billions of dollars but also at least a decade to rebuild the industry system from scratch. Yet Trump's term is only four years — by the time ships are built, the flowers would have withered.

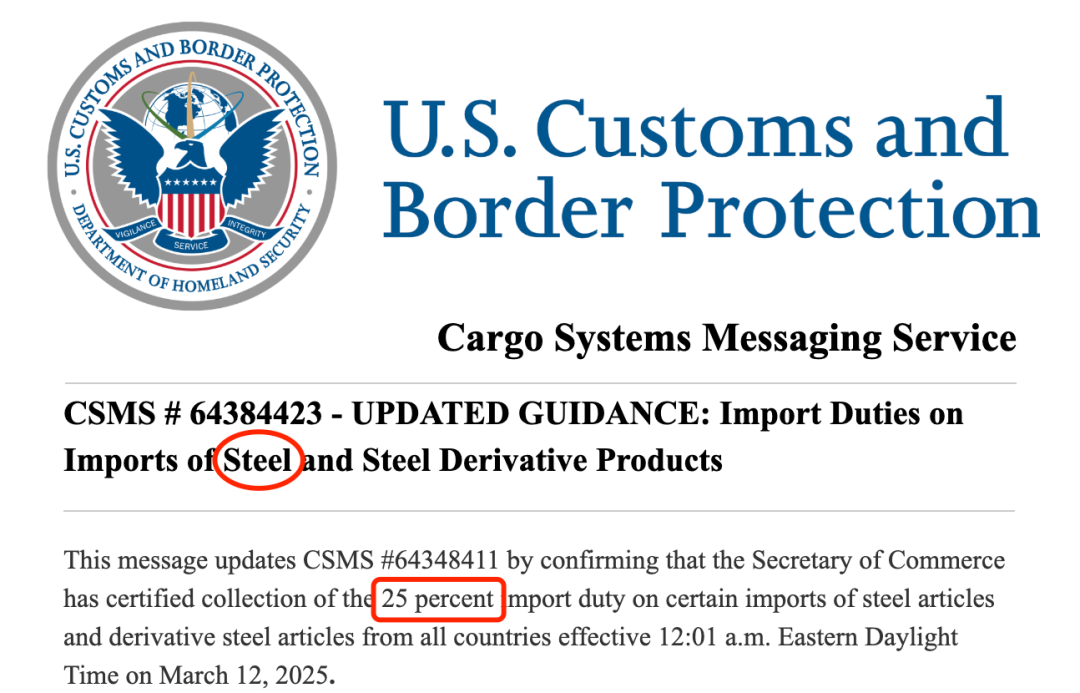

25% Tariff on Steel

Moreover, shipbuilding cannot do without steel raw materials. However, Trump's recent tariff policies (Section 232 took effect on March 12, imposing 25% tariffs on imported steel and 200% tariffs on Russian aluminum) have already sent steel prices soaring, making the revival of U.S. shipbuilding a "hellish" challenge. This also indicates that he is not particularly interested in shipbuilding.

It's like a homeroom teacher forcing everyone to copy homework from a poor student, only to find the poor student has submitted a blank paper.

Furthermore, the global shipping industry cannot do without Chinese shipbuilding.

Over the past year, China's shipbuilding completion volume accounted for 55.7% of the global total, ranking first for 15 consecutive years. In other words, one out of every two new ships built globally is "Made in China."

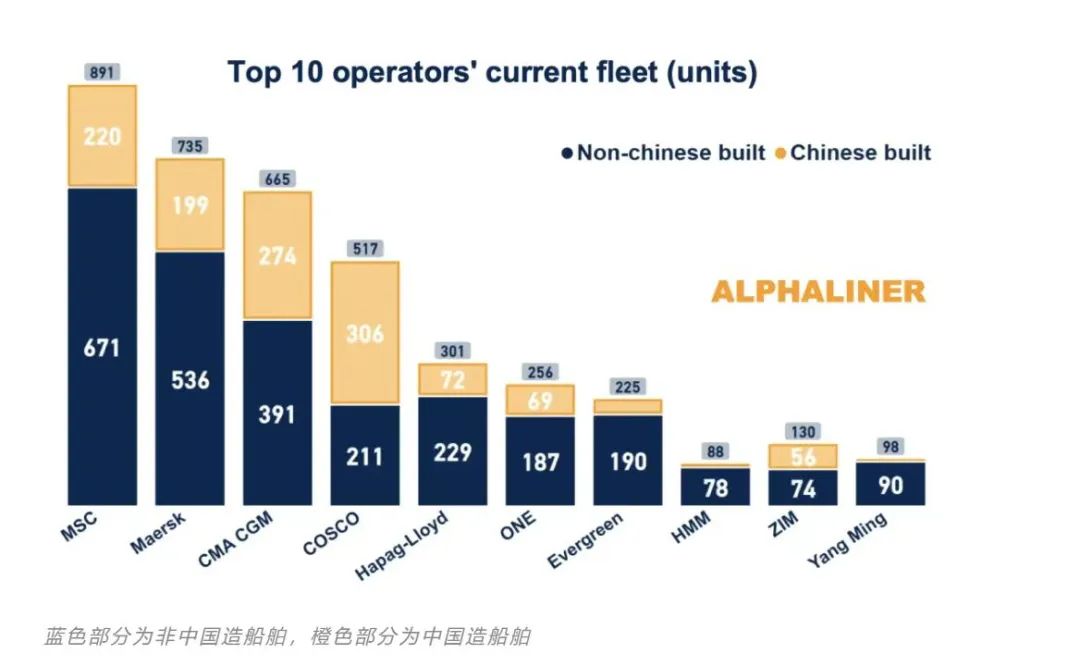

Source: Alphaliner

Major shipping companies: All new ship orders for COSCO, and 60% of its existing fleet, are built by Chinese shipyards; ZIM 43%; CMA CGM 41%;

Absolute numbers: CMA CGM has as many as 274 "Chinese-built" vessels; MSC has 220; Maersk has 199;

New ship orders: 93% of MSC's new orders, 92% of Hapag-Lloyd's, 70% of Maersk's, and 52% of CMA CGM's are from China.

With these proportions, separating shipping companies from Chinese shipbuilding would not just be cutting off an arm — it would be dismemberment. So, shipping companies will likely "change their disguise" and continue operating: for example, registering vessels in Panama, flying Liberian flags, hiring Indian crew, and claiming to have leased the vessels from Japanese owners.

At that point, the array of flags on vessels at U.S. ports might be even more varied than those in front of the United Nations.

Finally, the U.S. itself may not be able to withstand the inflationary pressure.

In 2024, total U.S. container imports reached 28 million TEUs, of which 20 million TEUs came from Asia. Under the bill's standards, most of these vessels would be subject to service fees.

The Peterson Institute predicts that for every 15% increase in U.S.-China shipping costs, U.S. inflation will rise by 0.8%.

Wealth does not materialize out of thin air. The increased port service fees will ultimately be borne by U.S. consumers, undermining the inflation control the Fed has painstakingly achieved.

Trump is unlikely to be unaware of this logic. Last year, he threatened 60% tariffs, but now it's a gradual 10%, 10% approach. It's negotiation psychology — smash the cup and see if you flinch. If that doesn't work, probe little by little to find your limits.

Additionally, the U.S. itself is suffering from severe inflation and cannot withstand aggressive measures. Whether it's raising tariffs or imposing port fees, it is expected to be done in phases to test economic reactions before determining the dosage.

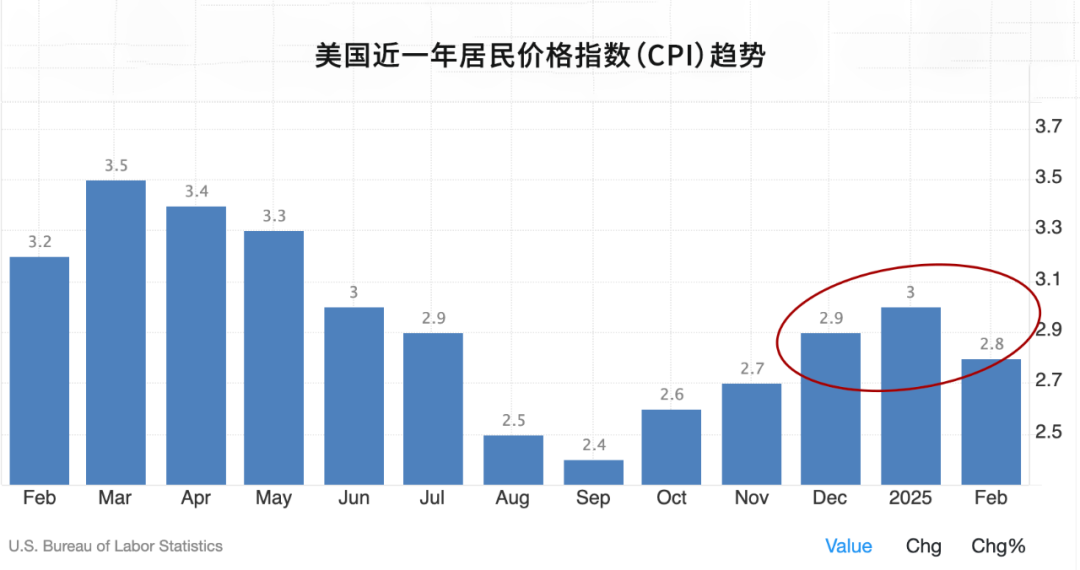

In the past few months, the U.S. inflation rate has been persistently around 3%, rising for five consecutive months above the Fed's 2% target. The midterm elections are in November 2026. To secure Congress, Trump must stabilize the economy. Otherwise, losing seats in the Senate and House would make it impossible to push through any policies later on.

Lose tariffs, lose a lot.

Lose seats, lose everything.

From T86 to Section 301, from new tariffs to port fees, these are all reflections of the ongoing global supply chain restructuring. For cross-border e-commerce, the rules of survival in the market are constantly changing. But just as water always finds a crack to flow through, a way will always be found when one reaches the end of the road.