Good news came from Geneva on Monday afternoon.

At 9:00 a.m. on May 12, Swiss time, the China-US talks reached an important consensus, officially issuing the "China-US Geneva Joint Statement on Economic and Trade Consultations":

Both sides committed to taking the following measures by May 14, 2025:

The United States will:

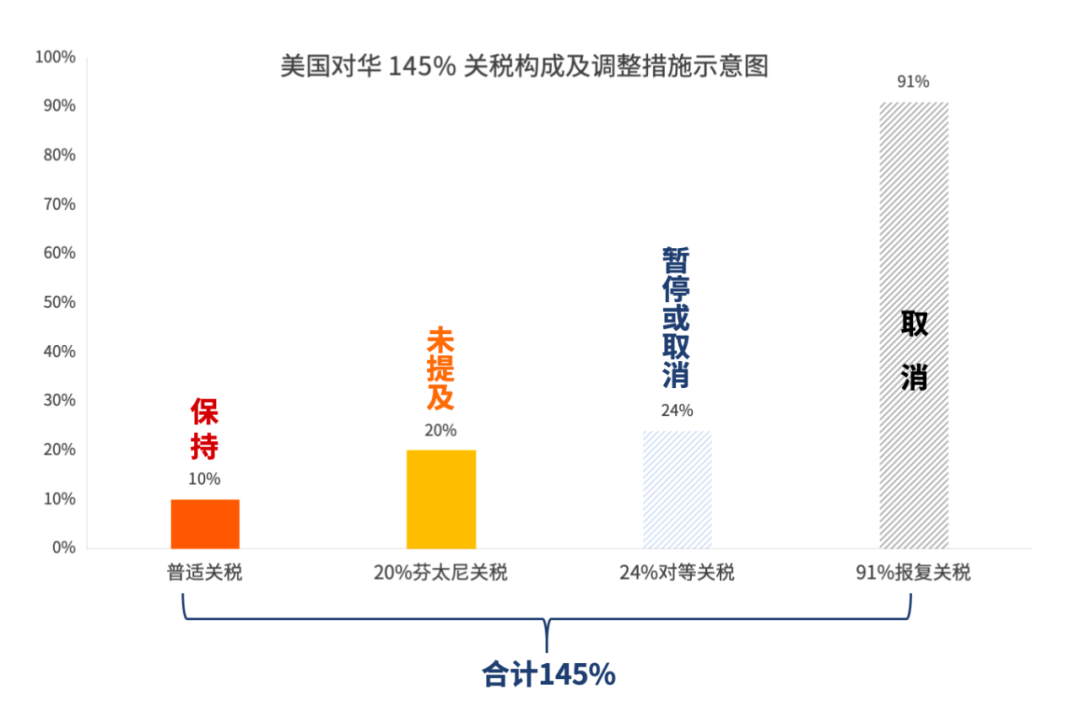

(1) Modify the ad valorem tariffs imposed on Chinese goods (including those from the Hong Kong Special Administrative Region and the Macau Special Administrative Region) as stipulated in Executive Order No. 14257 of April 2, 2025, by suspending the 24% tariff for an initial period of 90 days, while retaining the remaining 10% tariff on these goods as provided for in the Executive Order;

(2) Eliminate the additional tariffs imposed on these goods under Executive Order No. 14259 of April 8, 2025, and Executive Order No. 14266 of April 9, 2025.

China will:

(1) Correspondingly modify the ad valorem tariffs imposed on US goods as stipulated in Tariff Commission Announcement No. 4 of 2025, by suspending the 24% tariff for an initial period of 90 days, while retaining the remaining 10% tariff on these goods, and eliminate the additional tariffs imposed on these goods under Tariff Commission Announcements No. 5 and No. 6 of 2025;

(2) Take necessary measures to suspend or eliminate non-tariff countermeasures against the United States implemented since April 2, 2025.

Looking at the briefing released by the White House, the message is essentially the same.

In simple terms:

· The US eliminated a total of 91% of the additional tariffs, and China correspondingly eliminated 91% of its retaliatory tariffs;

· The US suspended the 24% "reciprocal tariff," and China correspondingly suspended its 24% retaliatory tariff.

· The current remaining tariffs are the 10% baseline tariff + the 20% "fentanyl tariff," which was neither mentioned nor eliminated.

Conclusion: Far better than expected.

For easier understanding, see the diagram below:

Last night, the whole world was watching the outcome of the China-US talks. Everyone can now breathe a sigh of relief. The next step is to let actions speak.

The cross-border e-commerce community is also buzzing. Tonight, we can all sleep well.

01

Looking at the Joint Statement, some details have yet to be finalized, such as the fate of the "90-day suspension of the 24% tariff." However, the "91% retaliatory tariff" that everyone was most concerned about has been eliminated.

For cross-border e-commerce, this is a positive turning point:

At the very least, both sides have opened the door to dialogue, bringing abnormal trade rules back to a normal negotiating framework and bringing outrageous tariffs back to a level where business can be done.

To translate, "The two sides will establish a mechanism to continue consultations on economic and trade relations" means that from now on, when the "Don" calls, someone on the other end will answer.

At this point, we might as well remain calm.

Both "quick victory" and "quick defeat" mentalities are unwise. Given Trump's businessman mindset, his age of 79, and his countless schemes, you never know whether he's playing black, white, or even checkers until his piece hits the board.

He is also exceptionally good at taking back his moves.

Today, May 12, is also a special day for the Chinese people.

Whether it's natural disasters or man-made calamities, nothing is insurmountable. Just as manufacturing strength can be agreed upon in shipping containers, tariff rates can certainly be agreed upon at the negotiating table.

Truth lies within the range of the J-10C. With tariffs reduced this much this time, everyone owes a deep bow to the "Ten."

02

May is also the most critical month for the United States.

Given Trump's personality, he never reasons when reason could work. If he ever does reason with you, it must be because he can no longer hold on.

America's current problems are quite serious.

The foreign ownership rate of US Treasury bonds was 50% in 2018, dropped to 42% in 2019, 35% in 2020, 30% in 2023, and only 23.5% in 2024. The world is dumping US debt.

In fiscal year 2025, the US federal government's revenue is approximately $5.2 trillion, but expenditures are reaching $7 trillion. Moreover, in June 2025, Trump will face $6.5 trillion in maturing Treasury bonds — $5.5 trillion more than last year.

Inflation is stirring in May, and bonds are maturing in June. These are the pressures driving Trump to seek negotiations and make concessions: "You tell me not to worry, but I really am worried."

Earlier this month, the Federal Reserve once again indicated that it would "hold off on cutting interest rates," citing the imminent risks of rising inflation and unemployment due to Trump's blanket tariff increases.

After the Fed signaled a "wait-and-see" approach, market institutions forecast that the number of rate cuts in 2025 would be reduced to "no more than three," with the benchmark rate decreasing by less than 75 basis points. The earliest rate cut would also be postponed until at least July.

If the tariff standoff continues, it will push up US inflation, making the Fed even less likely to cut rates, leading to higher Treasury yields, greater debt pressure, and ultimately a "triple sell-off" in US stocks, bonds, and the dollar. This is the underlying reason for Trump's sudden change in tone — he can no longer hold on.

Therefore, to stabilize prices, the US must lower tariffs, allow large volumes of cheap Chinese goods to enter, then proceed with interest rate cuts to issue new Treasury bonds to pay off old debt.

From the perspective of alleviating inflation, this also represents an ongoing era of opportunity and long-term value for cross-border e-commerce in the US.

03

According to the "Haishin Observation" perspective:

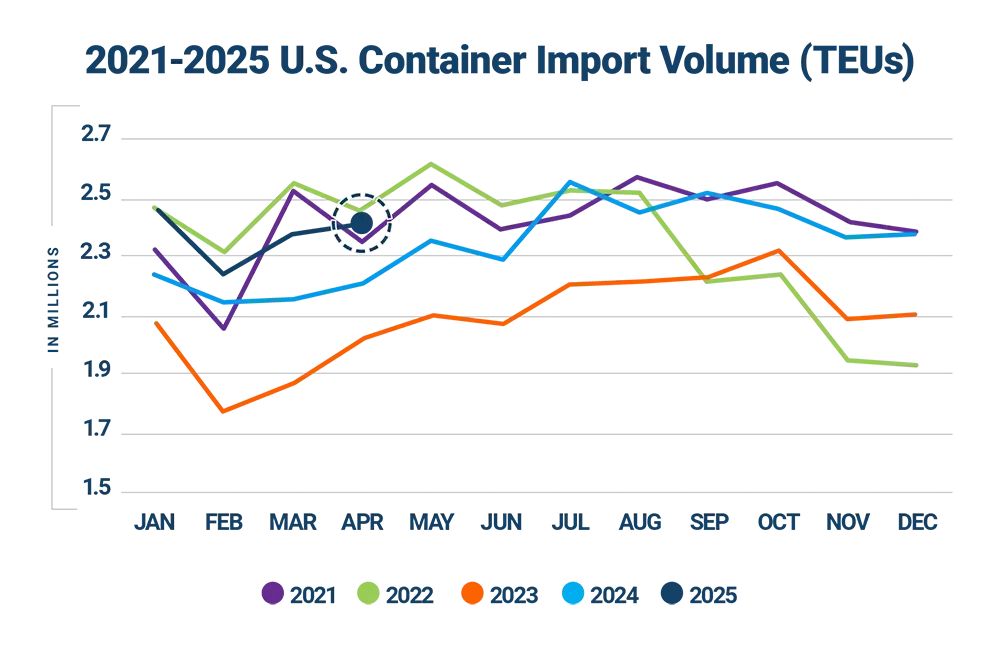

The NRF (as of April 9) predicted that US import cargo volume would fall by 20% in the second half of 2025, with the full-year decline possibly reaching 15%. The 19 consecutive months of growth may end in May, with July and August expected to see year-over-year declines as high as 27%.

The actual situation is even worse than this forecast. In the week after "Liberation Day," US import container volume fell to 500,000 TEUs, hitting a two-year low. The continued year-over-year growth is expected to end early in April, a full month earlier than predicted.

Combined with shipment data from China and Southeast Asia, US retail and wholesale inventory growth is expected to slow and peak in April. Since import container volume leads local inventory levels by about one month, this means the US will experience the first inventory shortage turning point in May.

Tariffs were increased from 20% to 145% in just one month. US businesses had no time to replenish inventory. Moreover, the first quarter is not when businesses have the most stock on hand. Existing inventory can only barely sustain them for one or two months.

Conclusion: Inventory for certain categories in the US will run out in 1-2 months. Without tariff reductions, the goods will be gone.

"The tariff war is an inventory war." US retailers have empty shelves and insufficient cash. This is another reason why the US was so eager to negotiate in May.

04

Future Outlook:

According to data from the General Administration of Customs, China's total goods trade import and export value in April was 3.84 trillion yuan, a year-on-year increase of 5.6%. Among this, exports reached 2.27 trillion yuan, up 9.3% year-on-year.

However, due to the extremely high tariffs in April, China's exports to the US fell by 21% year-on-year that month. However, exports to ASEAN grew by 12.6% year-on-year, and exports to the EU grew by 6% year-on-year. This is partly related to shippers optimizing their supply chain layouts and focusing on new markets.

From the perspective of US container imports, from February to April, US container import volume remained strong, growing for three consecutive months. April imports reached 2,410,371 TEUs, a month-on-month increase of 1.2% and a year-on-year increase of 9.1%, marking the second time this year that imports exceeded 2.4 million TEUs.

Among this, imports from China increased by 5.4% month-on-month and 6.2% year-on-year, accounting for 33.4% of total US container imports.

Imports from China saw the largest increase, adding 41,000 TEUs. This may be related to stockpiling ahead of the tariff implementation.

There might have been a huge V-shaped gap in exports in May. However, with the release of the "China-US Geneva Joint Statement," tariffs between the US and China have been significantly reduced by 91%. Even though the 24% "reciprocal tariff" remains unresolved, it still gives sellers a strong boost of confidence.

It is expected that there will be a significant wave of stockpiling in the coming months, "making up for" the shortages caused during the tariff war in April. This will coincide with the traditional peak season stockpiling. At that time, we should be prepared for potential impacts such as rising sea freight rates, tight container space, port congestion, and exchange rate fluctuations.

Due to time constraints and the fact that developments have exceeded expectations, we will continue to share other interpretations or policies regarding US tariffs in the future.

In the Geneva statement, T86 was not mentioned. The fate of "full managed" services remains uncertain. We look forward to the next round of negotiations bringing more good news for Chinese sellers.

We stand by our statement: Tariffs cannot contain cross-border e-commerce.

HGC Haishin Warehouse firmly believes in the future of cross-border e-commerce and remains optimistic about Chinese enterprises going global.